Initiating Coverage |Kitchen Appliances

August 17, 2018

TTK Prestige Ltd.

BUY

CMP

`6237

Growth to revive…

Target Price

`7500

TTK Prestige (TTK) is the leading brands in kitchen appliances with 40%+

Investment Period

12 Months

market share in organized market. It has evolved from being a single product

company to a multi product company offering an entire gamut of kitchen and

home appliances (600+ products). It expects to double its revenue in the next

Stock Info

5 years backed by revival in consumption demand, new 5 cr LPG connections

Sector

Kitchen Appliances

under the Ujjawala Scheme, inorganic expansion and traction in exports.

Market Cap (` cr)

7,210

Leader in product innovation: TTK has been the pioneer in launching new

Net Debt (` cr)

-

products like non-stick cookware, cookers. It has been launching 50-100 new

Beta

0.6

products every year for the past few years which has boosted its revenue growth

52 Week High / Low

8911/5612

while its peers like Hawkins suffered stagnation. It has also launched a economy

range - ‘Judge Cookware’ to capture the untapped demand especially at the

Avg. Daily Volume

3,576

bottom end of the pyramid. It is also expecting good growth in cleaning solutions.

Face Value (`)

10

BSE Sensex

37,663

Favorable market dynamics: Indian Kitchen appliances industry is valued at

`12000cr+ where TTK commands > 15% market share. After posting a couple of

Nifty

11,384

subdued years, we feel that the company is now in sweet spot with revival in

Reuters Code

TTKL.BO

consumption demand, especially rural. 5 cr new LPG connections have rekindled

Bloomberg Code

TTKPT.IN

demand for pressure cookers/cookware. TTK is also scouting for inorganic

opportunities to support its growth plans.

Shareholding Pattern (%)

Strong balance sheet: TTK has been aggressively investing in its manufacturing

Promoters

70.4

capabilities and has invested over ` 500 cr in the last 7-8 years. Looking at

buoyant expected demand, it is incurring a capex of ~`250 cr over FY2019-21.

MF / Banks / Indian Fls

8.4

This capex is to be internally funded from its robust operating cash flows. With

FII / NRIs / OCBs

10.0

improving profitability and debt free status, its return ratios are likely to improve.

Indian Public / Others

11.2

Outlook and valuation: We expect TTK to report a CAGR of 18.6%/24.5% in

revenue/PAT respectively over FY2018-20E. It is currently trading at a P/E of 29x

Abs. (%)

3m

1yr

3yr

FY2020E EPS which is at discount to its 5 year average PE multiple of 40x. Hence,

we initiate coverage on the stock with a BUY and Target Price of `7500 (35x

Sensex

6.4

1.0

35.1

FY2020E EPS), an upside of 21% from the current levels.

TTK Prestige

5.3

1.5

60.0

Key Financials (Consolidated)

Y/E March (` cr)

FY2016

FY2017

FY2018E

FY2019E

FY2020E

Price Chart

Net Sales

1,559

1,837

1,982

2,371

2,788

% chg

12.3

17.8

7.9

19.6

17.6

Net Profit

115.6

150.7

164.5

205.4

247.4

% chg

25.2

30.3

9.2

24.9

20.4

OPM (%)

11.8

11.4

12.7

13.4

13.6

EPS (Rs)

100.0

130.3

142.3

177.7

214.0

P/E (x)

62.4

47.9

43.8

35.1

29.1

P/BV (x)

0.4

0.3

0.3

0.2

0.2

Source: Company, Angel Research

RoE (%)

16.0

17.6

16.1

17.3

17.8

RoCE (%)

22.4

19.0

19.6

22.0

22.7

Nidhi Agrawal

EV/Sales (x)

4.6

3.9

3.6

3.0

2.5

022 - 3935 7800 Ext: 6872

EV/EBITDA (x)

38.8

34.2

28.1

22.1

18.3

Source: Company, Angel Research; Note: closing price of 16th August , 2018

Please refer to important disclosures at the end of this report

1

Initiating Coverage | TTK Prestige

TTK prestige in charts

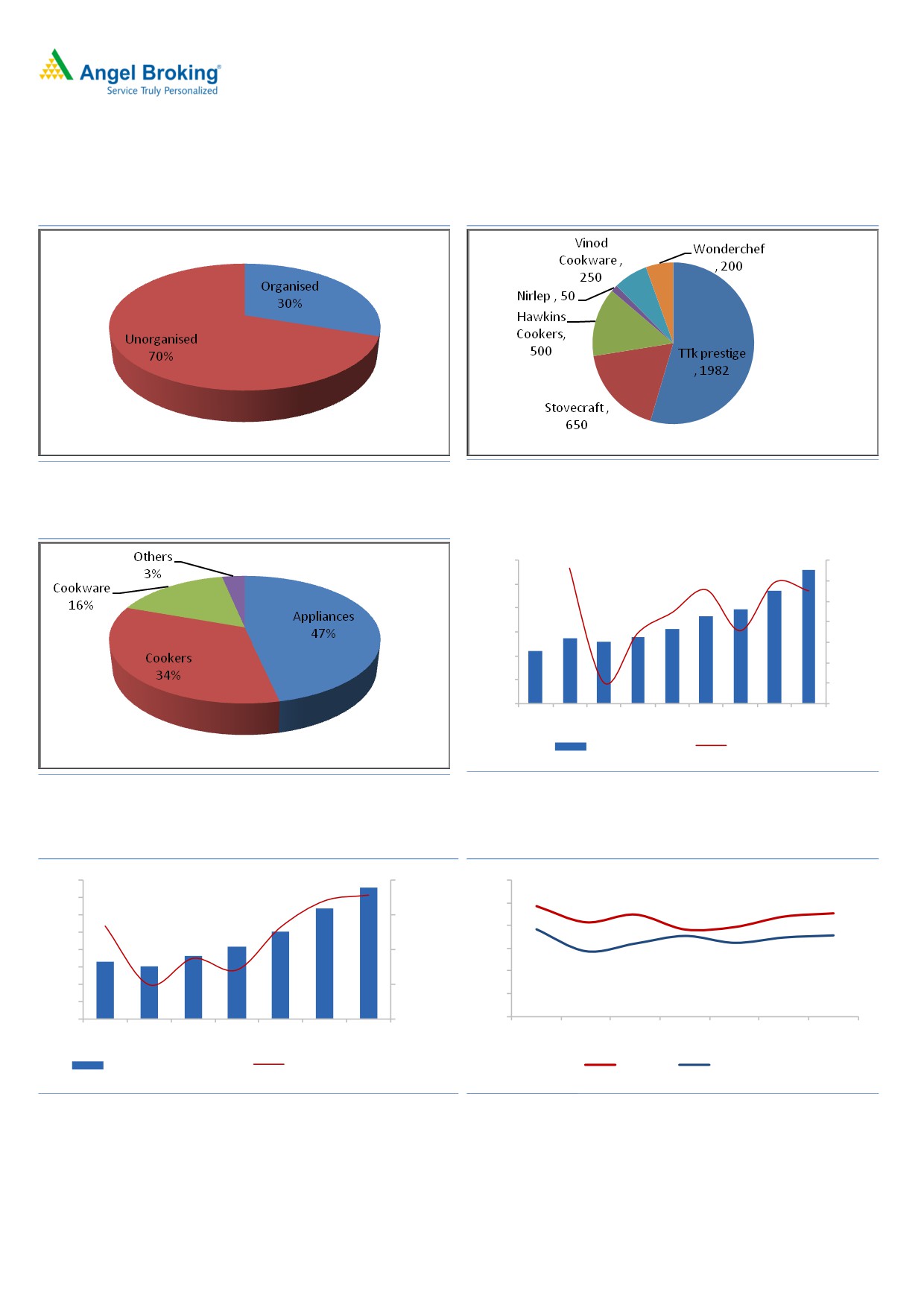

Exhibit 1: Kitchen appliances industry break up

Exhibit 2: Top 6 players by their revenue (`cr)

Source: Industry, Angel Research

Source: Industry, Angel Research

Exhibit 3: TTK’s product wise revenue break up

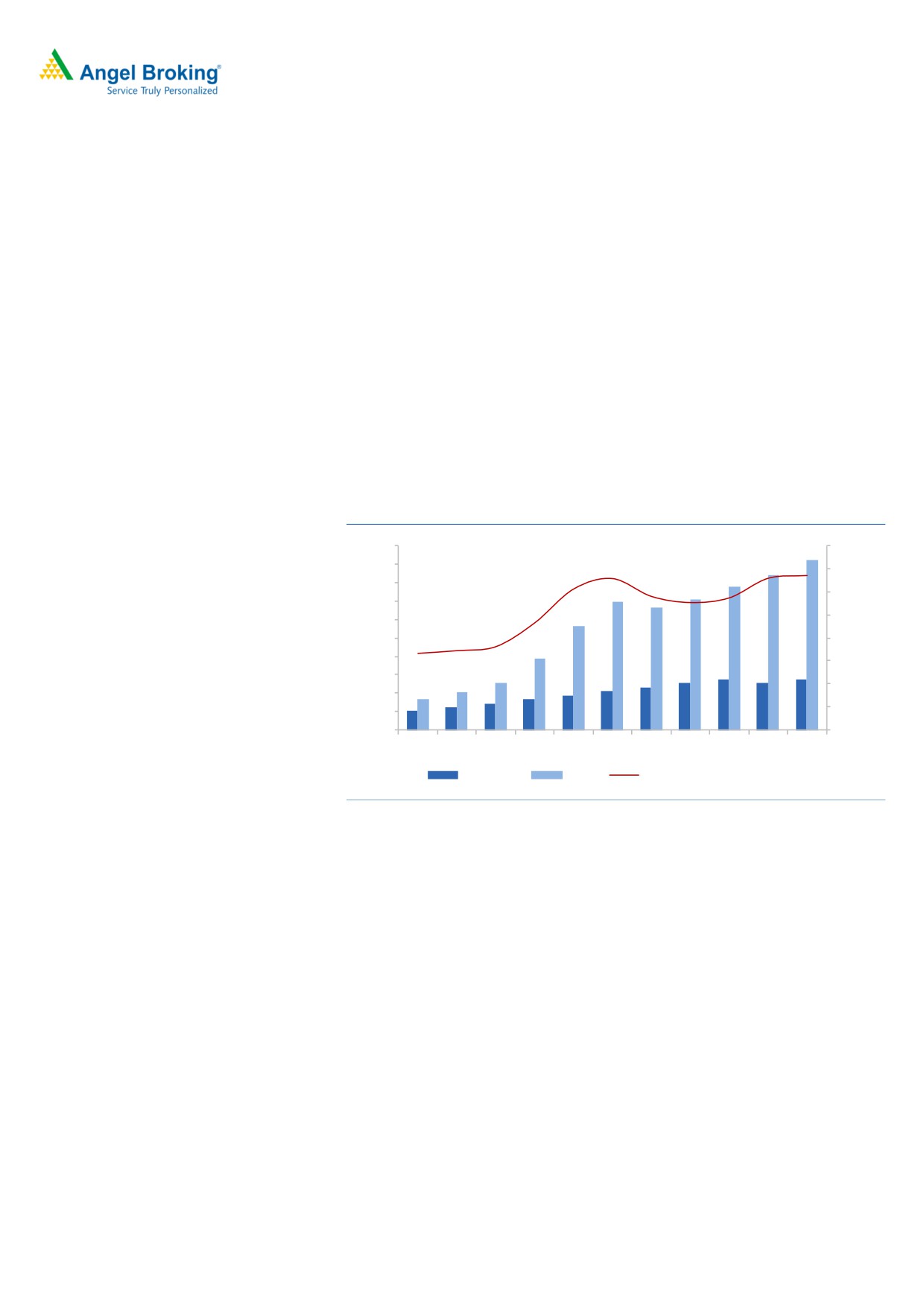

Exhibit 4: Sales growth to rekindle over next few years

3000

25%

2500

20%

15%

2000

10%

1500

5%

1000

0%

500

-5%

0

-10%

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

Net Sales- ` cr

YoY chg (%)

Source: Company, Angel Research

Source: Company, Angel Research

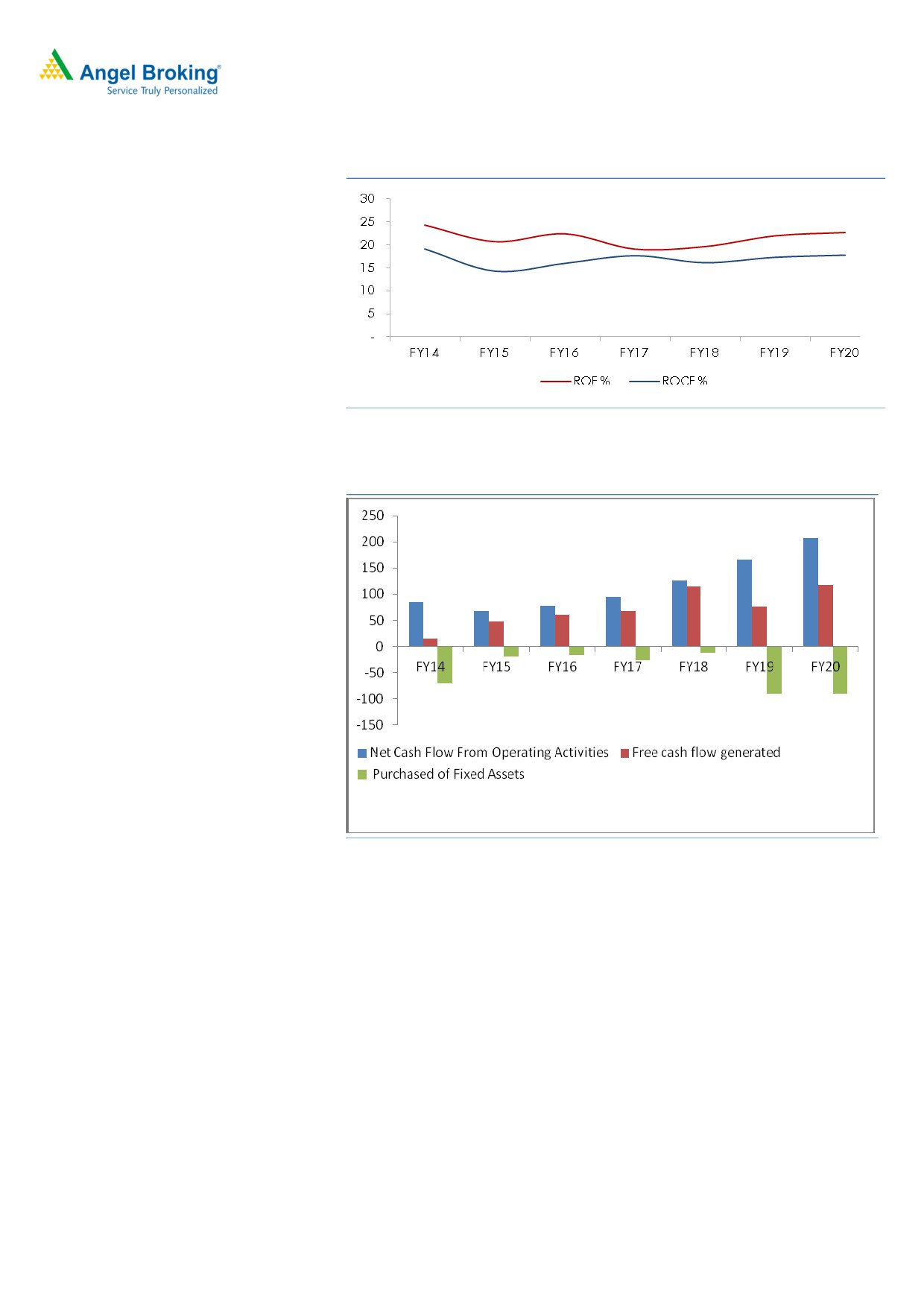

Exhibit 5: Improving its margin profile

Exhibit 6: Stable return ratios

400

14.0%

30

350

25

300

13.0%

20

250

200

12.0%

15

150

10

100

11.0%

5

50

0

10.0%

-

FY14

FY15

FY16

FY17

FY18

FY19

FY20

FY14

FY15

FY16

FY17

FY18

FY19

FY20

Operating profit (` cr)

Operating margin (%)

ROE %

ROCE %

Source: Company, Angel Research

Source: Company, Angel Research

August 17, 2018

2

Initiating Coverage | TTK Prestige

Company background

Founded in 1928, the TTK group spans 30 product categories with 7 group

companies and a turnover `3000cr+. TTK Prestige is its flagship company. It

started manufacturing in 1949 by setting up a unit near Bangalore. TTK was

incorporated as a private limited company in 1955 and it became a public

limited company in 1988. It remained a single product company till 1990. The

company is known for its manufacturing and innovations, be it distributing

pamphlets from helicopters in the fifties or introducing the exchange schemes.

Exhibit 7: Evolved from single product company

to a well diversified multi-product portfolio

Source: Company

Exhibit 8: Time line of the company

Year

Event/ development

1955

Incorporation

1959

First manufacturing unit in Bangalore

1981

Second manufacturing unit in Hosur

Till 1990

A single product company-just aluminum outer lid pressure cookers-dominant in southern India

1990-94

Launch of pressure cookers and non-stick cookware

1990s

Export thrust-launch of manttra brand

2000-03

Period of turbulences-yet bold initiatives laying the foundation for brand extension and explosive growth

Transformation into a total kitchen solution provider lead by innovations like induction tops, apple cookers, microwave

2006-10

pressure cookers and a host of appliances

2011

Largest capacity expansion initiatives to back the above vision

2012

Alliances with global high end brands entered for high end cookware/store ware/water filters/gas tops

2016

Entered new horizons -UK acquisition & cleaning solutions

Source: Company, Angel Research

August 17, 2018

3

Initiating Coverage

| TTK Prestige

Investment Rationale

Leader in product innovation

TTK has been the first mover in introducing many pioneering products like non-

stick cookware, pressure cookware etc which has led to company garnering over

40% market share in organized market. Introduction of new appliances led to

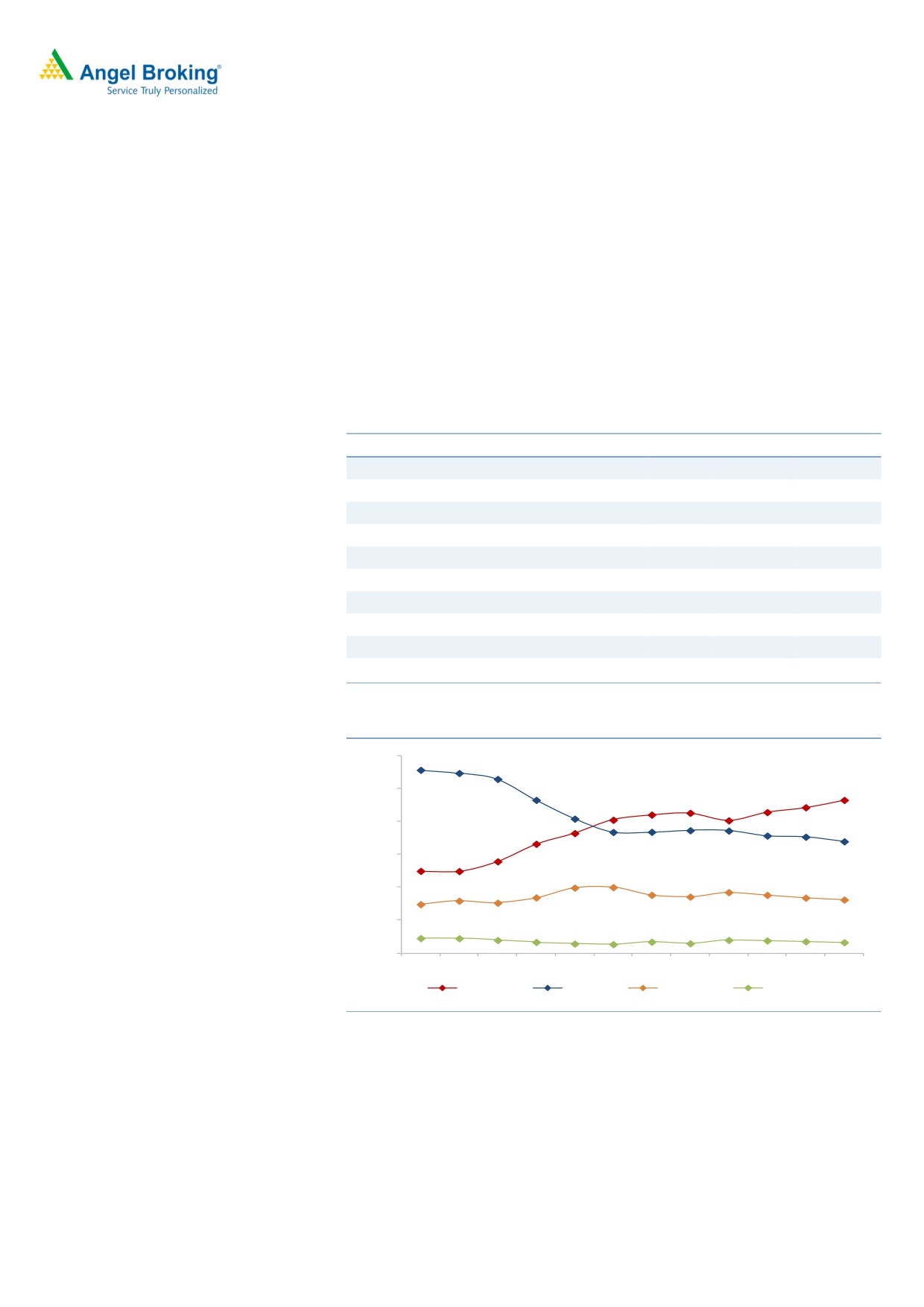

reduction in revenue contribution from pressure cookers to 34% in FY2018 from

past level of 50%. The company is rebranding its exclusive branded outlets (17% of

sales) from ‘Prestige Smart Kitchen’ to Prestige Exclusive’ to re-energize its

traditional channels to offers its new launches. It has also launched a economy

range - Judge Cookware to capture the untapped demand especially rural at the

bottom end of the pyramid.

Exhibit 9: Product-wise revenue break up

` cr

FY08

FY14

FY18

Appliances

85

564

861

Cookers

186

494

628

Cookware

54

227

300

Others

15

39

60

Total Standalone revenue

340

1,323

1,849

As a % of revenue

Appliances

24.9%

42.6%

46.6%

Cookers

54.8%

37.3%

34.0%

Cookware

15.9%

17.1%

16.2%

Others

4.5%

2.9%

3.2%

Source: Company, Angel Research

Exhibit 10: Successfully diversified away from cookers segment

60.0%

50.0%

40.0%

30.0%

20.0%

10.0%

0.0%

FY07

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

Appliances

Cookers

Cookware

Others

Source: Company, Angel Research

Growth to revive

The company has been annually launching 50-100 new products for the past few

years which led to diversification in its product portfolio away from pressure

cookers. In Q1FY2019 itself, there were 30 new launches and expects to launch

100 products in FY2019. Growth has revived un Q1FY2019 with 17.5% yoy

growth which is expected to continue for few more quarters.

After posting a couple of subdued years, we feel that the company is now in sweet

spot with revival in consumption demand especially rural, improving outlook for

August 17, 2018

4

Initiating Coverage | TTK Prestige

exports and the new 5 cr LPG connections in India which rekindle demand for

pressure cookers and cookware. It is also expecting exponential growth in cleaning

solutions and expects the segment revenue to grow from ~`23 cr in FY2018 to ~

`400 cr from in next five years.

Exhibit 11: Revenue growth to revive after a brief spell of slowdown

3000

25%

2500

20%

15%

2000

10%

1500

5%

1000

0%

500

-5%

0

-10%

FY12

FY13

FY14

FY15

FY16

FY17

FY18

FY19

FY20

Net Sales- ` cr

YoY chg (%)

Source: Company, Angel Research

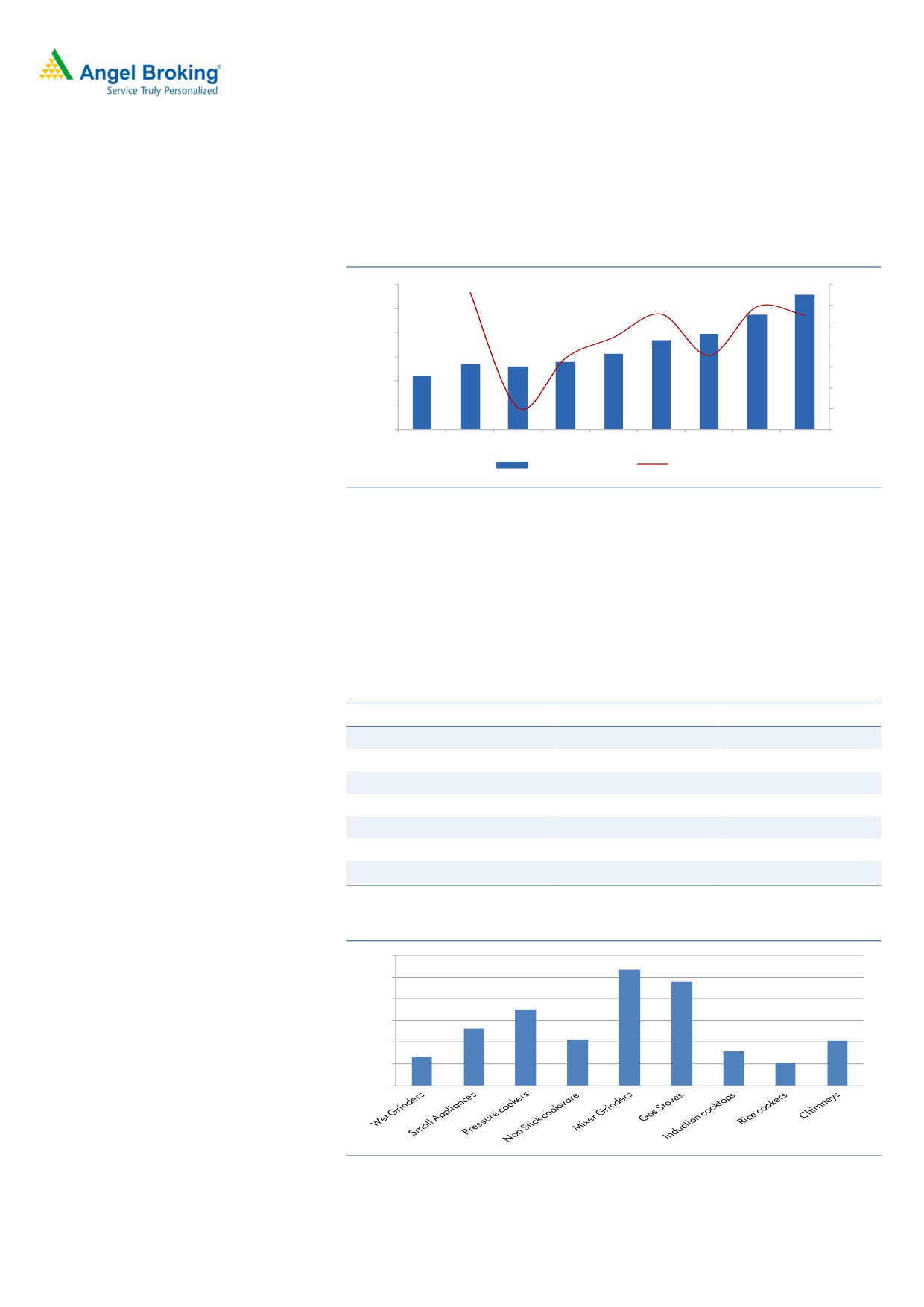

Favorable market dynamics

Indian Kitchen appliances industry is valued at ~`12000cr where TTK commands

over 15% market share. Top 6 branded players form about 30% of market. The

2nd player - StoveKraft and 3rd player- Hawkins Cookers is having 1/3rd and 1/4th

of TTK’s revenue. Many other players have faced revenue fall like Nirlep for lack of

innovation whose market share has been acquired by TTK prestige.

Exhibit 12: Top 6 players forms ~30% of market

Revenue- ` Cr

Market Share %

TTK prestige

1982

17%

Stovecraft (Pigeon and Gilma brand)

650

5%

Hawkins

500

4%

Nirlep *

50

0%

Vinod ware

250

2%

Wonder chef

200

2%

Total organized market

3,632

30%

Source: Companies, media reports

* acquired by Bajaj Electrical in June 2018

Exhibit 13: Market size (` Cr) for TTK’s products

3000

2500

2000

1500

1000

500

0

Source: Company’s 2016 presentation

August 17, 2018

5

Initiating Coverage | TTK Prestige

Ujjawala scheme -big boost to pressure cookers and cookware

Twenty-eight months since its launch, Pradhan Mantri Ujjwala Yojana (PMUY) has

already achieved the initial target of providing 5-crore LPG connections to BPL

households, and considering its success in the current year, the government has

revised the target to 8 crore with a budgetary allocation of `12,800 crore. As on

July 1, 2018, there are 23.5 cr LPG consumers in the country. As soon as a

household gets a LPG stove connection, one of the first appliances they buy is a

pressure cooker.

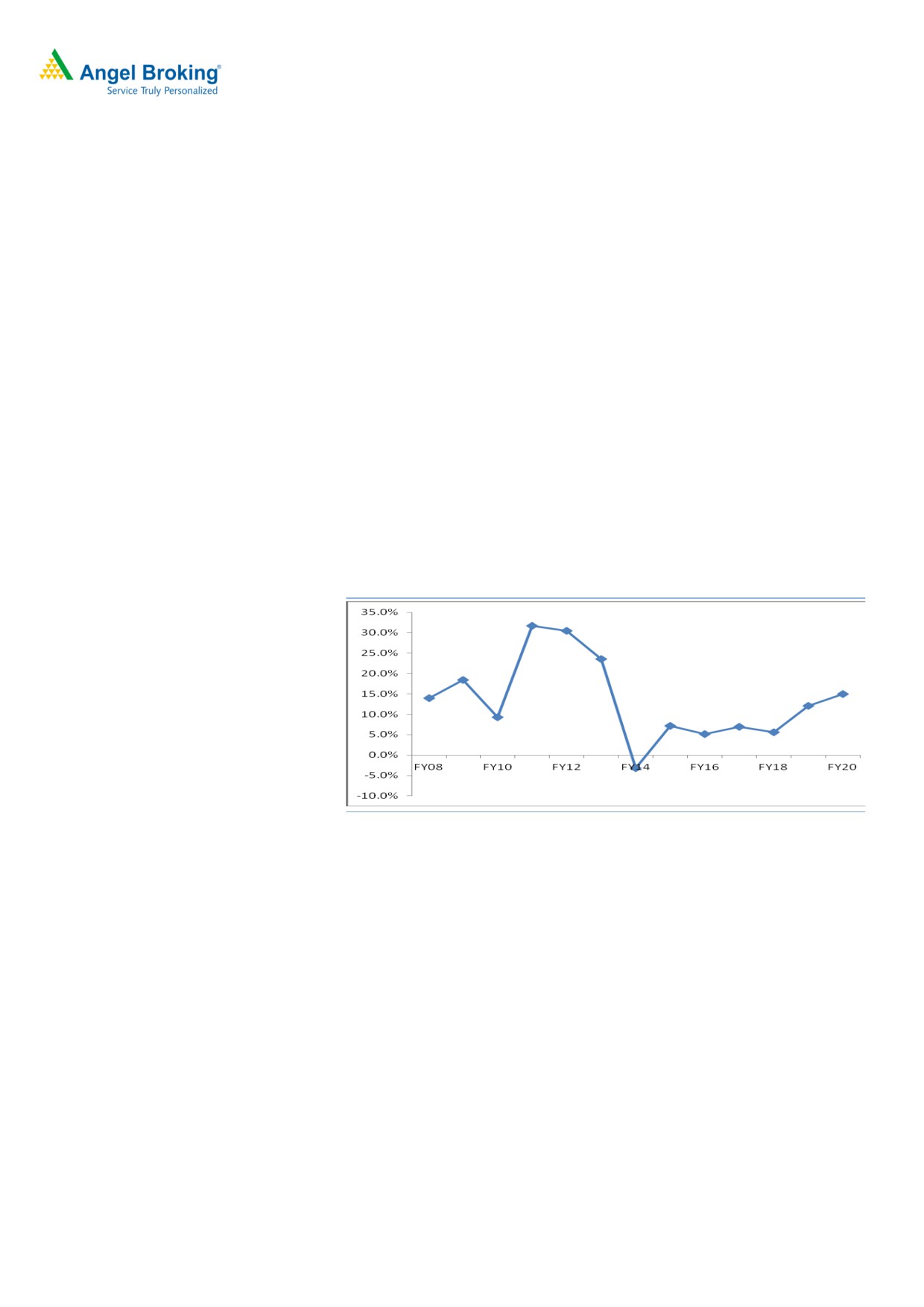

Pressure cooker industry to grow at double digit for next few years

Pressure cooker industry is estimated at `1,500-2,000 crore and has as many as

250 brands. TTK with over 35-40% market share is the leader with Hawkins and

United among the other key organised brands in the market. It is a mature market

and was seeing a single-digit growth of 5-6 % till recently which has now started

seeing a double-digit growth. While the penetration of pressure cookers is nearly

90% in urban regions, in rural areas it is just ~30 %. But Ujjwala seems to be

opening up the market in rural areas as well. TTK reported a 17.5% yoy growth in

pressure cooker in Q1FY2019 and expects similar run rate for next few quarters.

Exhibit 14: TTK ‘s pressure cookers sales to perk up

Source: Company, Angel Research Source: Company, Angel Research

Strong balance sheet and improving ratios

The company is debt free and generated free cash flow in excess of `100 cr in

FY2018. The company has been investing in increasing its manufacturing

capabilities and invested over `500 cr in last 7-8 years. It has reduced outsourcing

to 20% from past higher levels of 40-50% (FY2012) to reduce working capital cycle

and foreign currency exposure. Looking at buoyant demand for its products, it is

likely to incur a capex of ~`250 cr over FY2019-21. This capex is to be internally

funded from its robust operating cash flows. With improving profitability, its return

ratios are expected to improve.

August 17, 2018

6

Initiating Coverage | TTK Prestige

Exhibit 15: Return ratios remain stable

Source: Company, Angel Research

Exhibit 16: Robust operating cash flow would funs its capex

Source: Company, Angel Research

August 17, 2018

7

Initiating Coverage | TTK Prestige

Outlook

TTK has posted a CAGR of 18% in revenue over FY2008-18backed by 26% CAGR

in appliances segment whereas cookers and cookware segments showed a somber

CAGR of 13/19% respectively. Going ahead, we expect that appliances segment

will grow at higher 23% CAGR while cookers and cookware will also see a revival

with 13-15% CAGR over FY2018-20. Margins are largely expected to improve

marginally in line with better product mix and improving scale. In view of its strong

balance sheet, we expect that PAT will grow by 23% CAGR over the same period.

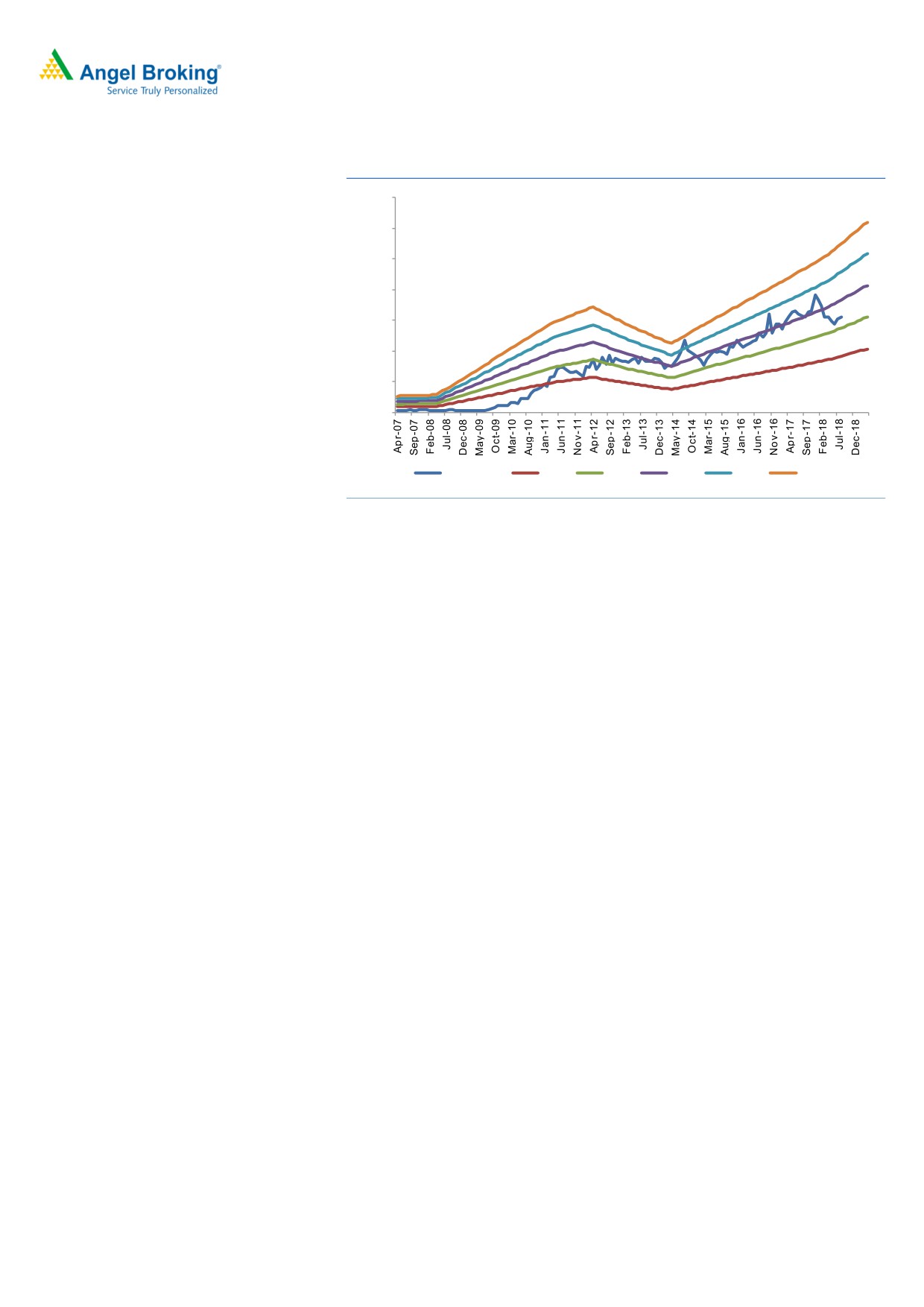

Competition analysis

TTK’s revenue was just 1.7x of that of Hawkins in FY2008. However, TTK widened

this gap at 3.3x in FY2018 by constantly introducing new products and distribution

expansion especially in North India. On the other hand, Hawkins remained

focused on the pressure cookers and cookware and hence suffered stagnation as

the cookers segment became highly penetrated segment.

Exhibit 17: TTK’s revenue growth outpaces its closet peer’s

400%

2000

1800

350%

1600

300%

1400

250%

1200

1000

200%

800

150%

600

100%

400

50%

200

0

0%

FY08

FY09

FY10

FY11

FY12

FY13

FY14

FY15

FY16

FY17

FY18

Hawkins

TTK

TTK as % of Hawkins revenue

Source: Companies, Angel Research

Valuation

The stock currently trades at a P/E of 29x FY2020E EPS which is at significant

discount to its past average 5 year PE multiple of 40x. Hence, looking at above

positive growth triggers, we initiate coverage on the stock with a BUY

recommendation and Target Price of `7500 (35x FY2020E EPS), an upside of 20%

from the current levels.

August 17, 2018

8

Initiating Coverage | TTK Prestige

Exhibit 18: Forward PE chart

14000

12000

10000

8000

6000

4000

2000

0

Share price

20 X

30 X

40 X

50 X

60 X

Source: Company, Angel Research

Risks and concerns

Abrupt fluctuations in its primary raw materials- Aluminum and steel whose prices

are linked to global commodity prices. Although the company has been able to

pass on the increase in raw material prices to consumers in the past owing to a

strong brand, any failure to do so in the future can adversely impact operating

margins.

Foreign exchange movement- The company imports raw materials and finished

goods from outside India as well as makes export sales to countries outside the

territories in which they operate from which exposes it to foreign currency risk.

Foreign currency exchange risks are managed by entering into forward contracts

against foreign currency vendor payables.

Excessive competition/ pricing war - TTK is competing with many different players

in different category. Many foreign players are also entering Indian markets which

could lead aggressive competition, pricing war. So far, TTK has gained market

share from its competition over the years with its innovative culture and growth

strategies.

August 17, 2018

9

Initiating Coverage | TTK Prestige

Income statement

Y/E March (` cr)

FY2016

FY2017

FY2018

FY2019E FY2020E

Total operating income

1,559

1,837

1,982

2,371

2,788

% chg

12.3

17.8

7.9

19.6

17.6

Total Expenditure

1,376

1,627

1,731

2,053

2,410

Raw Material

931

1,085

1,124

1,339

1,571

Personnel

114

138

159

185

217

Selling and Administration Expenses

313.8

374.0

421.0

497.9

585.5

Others Expenses

17

31

27

31

36

EBITDA

183

210

251

318

378

% chg

20.0

14.5

19.5

26.7

19.0

(% of Net Sales)

11.8

11.4

12.7

13.4

13.6

Depreciation& Amortisation

21

26

26

28

32

EBIT

162

184

225

289

346

% chg

21.4

13.4

22.3

28.6

19.5

(% of Net Sales)

10.4

10.0

11.4

12.2

12.4

Interest & other Charges

6

11

7

7

7

Other Income

10

11

141

20

25

(% of PBT)

6.2

5.9

39.4

6.6

6.9

Share in profit of Associates

-

-

-

-

-

Recurring PBT

167

184

359

302

364

% chg

25.1

10.2

95.3

(15.9)

20.4

Tax

51

33

96

97

116

(% of PBT)

30.7

18.1

26.6

32.0

32.0

PAT (reported)

116

151

263

205

247

Extraordinary Items

-

-

99

-

-

Less: Minority interest (MI)

0

0

0

0

0

PAT after MI (reported)

115

150

263

205

247

ADJ. PAT

116

151

165

205

247

% chg

25.2

30.3

9.2

24.9

20.4

(% of Net Sales)

7.4

8.2

8.3

8.7

8.9

Fully Diluted EPS (Rs)

100.0

130.3

142.3

177.7

214.0

% chg

25.2

30.3

9.2

24.9

20.4

Source: Company, Angel Research

August 17, 2018

10

Initiating Coverage | TTK Prestige

Balance sheet

Y/E March (` cr)

FY2016

FY2017

FY2018

FY2019

FY2020

SOURCES OF FUNDS

Equity Share Capital

12

12

12

12

12

Reserves& Surplus

711

842

1,008

1,175

1,381

Shareholders Funds

723

854

1,020

1,187

1,392

Equity Share Warrants

-

-

-

-

-

Total Loans

-

113

129

129

129

Deferred Tax Liability

-

-

-

-

-

Other liabilties

6.8

6.3

5.4

5.4

5.4

Total Liabilities

730

973

1,154

1,322

1,527

APPLICATION OF FUNDS

Gross Block

351

567

598

688

778

Less: Acc. Depreciation

21

58

108

137

169

Net Block

330

510

490

552

609

Capital Work-in-Progress

3

2

4

4

4

Investments

68

75

167

167

167

Current Assets

583

680

880

1,057

1,283

Inventories

325

380

437

523

615

Sundry Debtors

175

215

258

309

363

Cash

31

65

136

166

235

Loans & Advances

52

20

49

59

69

Other Assets

-

-

-

-

-

Current liabilities

238

281

373

445

522

Net Current Assets

346

400

507

612

761

Deferred Tax Asset

(29)

(35)

(42)

(42)

(42)

Total Assets

730

973

1,154

1,321

1,528

Source: Company, Angel Research

August 17, 2018

11

Initiating Coverage | TTK Prestige

Cash flow statement

Y/E March (` cr)

FY2016

FY2017

FY2018

FY2019

FY2020

Profit before tax

167

184

359

302

364

Depreciation

21

26

26

28

32

Change in Working Capital

0

0

0

(75)

(80)

Interest / Dividend (Net)

9

(0)

(6)

7

3

Direct taxes paid

(36)

(37)

(93)

(97)

(116)

Others

(83)

(78)

(159)

1

5

Cash Flow from Operations

78

94

127

166

207

(Inc.)/ Dec. in Fixed Assets

(17)

(26)

(12)

(90)

(90)

(Inc.)/ Dec. in Investments

11

(142)

9

20

25

Cash Flow from Investing

(6)

(168)

(3)

(70)

(65)

Issue of Equity

0

0

0

0

0

Inc./(Dec.) in loans

0

113

0

0

0

Dividend Paid (Incl. Tax)

0

0

0

0

0

Interest / Dividend (Net)

(2)

(8)

(75)

39

(31)

Cash Flow from Financing

(71)

106

(113)

0

(73)

Inc./(Dec.) in Cash

2

31

11

97

69

Opening Cash balances

25

27

58

69

166

Closing Cash balances

27

58

69

166

235

Source: Company, Angel Research

August 17, 2018

12

Initiating Coverage | TTK Prestige

Key Ratios

Y/E March

FY2016

FY2017

FY2018

FY2019

FY2020

Valuation Ratio (x)

P/E (on FDEPS)

62.4

47.9

43.8

35.1

29.1

P/CEPS

2.1

1.6

1.0

1.2

1.0

P/BV

0.4

0.3

0.3

0.2

0.2

Dividend yield (%)

0.4

0.4

0.5

0.5

0.6

EV/Sales

4.6

3.9

3.6

3.0

2.5

EV/EBITDA

38.8

34.2

28.1

22.1

18.3

EV / Total Assets

9.7

7.4

6.1

5.3

4.5

Per Share Data (`)

EPS (Basic)

100.0

130.3

142.3

177.7

214.0

EPS (fully diluted)

100.0

130.3

142.3

177.7

214.0

Cash EPS

118.1

152.6

250.1

202.1

241.9

DPS

22.0

27.0

30.0

33.0

36.3

Book Value

625.5

738.4

882.1

1,026.8

1,204.5

Dupont Analysis

EBIT margin

10.4

10.0

11.4

12.2

12.4

Tax retention ratio

0.7

0.8

0.7

0.7

0.7

Asset turnover (x)

2.5

2.2

2.3

2.4

2.5

ROIC (Post-tax)

18.0

18.2

19.5

20.0

21.0

Cost of Debt (Post Tax)

-

0.1

0.0

0.0

0.0

Returns (%)

ROCE

22.4

19.0

19.6

22.0

22.7

Angel ROIC (Pre-tax)

26.0

22.3

26.6

29.4

30.9

ROE

16.0

17.6

16.1

17.3

17.8

Turnover ratios (x)

Asset Turnover (Gross Block)

4.4

3.2

3.3

3.4

3.6

Inventory / Sales (days)

76

75

81

81

81

Receivables (days)

41

43

48

48

48

Payables (days)

93

94

121

121

121

Working capital cycle (ex-cash) (days)

24

24

7

7

7

Source: Company, Angel Research

August 17, 2018

13

Initiating Coverage | TTK Prestige

Research Team Tel: 022 - 39357800

DISCLAIMER

Angel Broking Limited (hereinafter referred to as “Angel”) is a registered Member of National Stock Exchange of India Limited, Bombay

Stock Exchange Limited, Metropolitan Stock Exchange Limited, Multi Commodity Exchange of India Ltd and National Commodity &

Derivatives Exchange Ltd It is also registered as a Depository Participant with CDSL and Portfolio Manager and Investment Adviser with

SEBI. It also has registration with AMFI as a Mutual Fund Distributor. Angel Broking Limited is a registered entity with SEBI for Research

Analyst in terms of SEBI (Research Analyst) Regulations, 2014 vide registration number INH000000164. Angel or its associates has not

been debarred/ suspended by SEBI or any other regulatory authority for accessing /dealing in securities Market. Angel or its

associates/analyst has not received any compensation / managed or co-managed public offering of securities of the company covered

by Analyst during the past twelve months.

This document is solely for the personal information of the recipient, and must not be singularly used as the basis of any investment

decision. Nothing in this document should be construed as investment or financial advice. Each recipient of this document should make

such investigations as they deem necessary to arrive at an independent evaluation of an investment in the securities of the companies

referred to in this document (including the merits and risks involved), and should consult their own advisors to determine the merits and

risks of such an investment.

Reports based on technical and derivative analysis center on studying charts of a stock's price movement, outstanding positions and

trading volume, as opposed to focusing on a company's fundamentals and, as such, may not match with a report on a company's

fundamentals. Investors are advised to refer the Fundamental and Technical Research Reports available on our website to evaluate the

contrary view, if any

The information in this document has been printed on the basis of publicly available information, internal data and other reliable

sources believed to be true, but we do not represent that it is accurate or complete and it should not be relied on as such, as this

document is for general guidance only. Angel Broking Limited or any of its affiliates/ group companies shall not be in any way

responsible for any loss or damage that may arise to any person from any inadvertent error in the information contained in this report.

Angel Broking Limited has not independently verified all the information contained within this document. Accordingly, we cannot testify,

nor make any representation or warranty, express or implied, to the accuracy, contents or data contained within this document. While

Angel Broking Limited endeavors to update on a reasonable basis the information discussed in this material, there may be regulatory,

compliance, or other reasons that prevent us from doing so.

This document is being supplied to you solely for your information, and its contents, information or data may not be reproduced,

redistributed or passed on, directly or indirectly.

Neither Angel Broking Limited, nor its directors, employees or affiliates shall be liable for any loss or damage that may arise from or in

connection with the use of this information.

Disclosure of Interest Statement

TTK PRESTIGE

1. Financial interest of research analyst or Angel or his Associate or his relative

No

2. Ownership of 1% or more of the stock by research analyst or Angel or associates or relatives

No

3. Served as an officer, director or employee of the company covered under Research

No

4. Broking relationship with company covered under Research

No

Ratings (Based on expected returns

Buy (> 15%)

Accumulate (5% to 15%)

Neutral (-5 to 5%)

over 12 months investment period):

Reduce (-5% to -15%)

Sell (< -15)

August 17, 2018

14